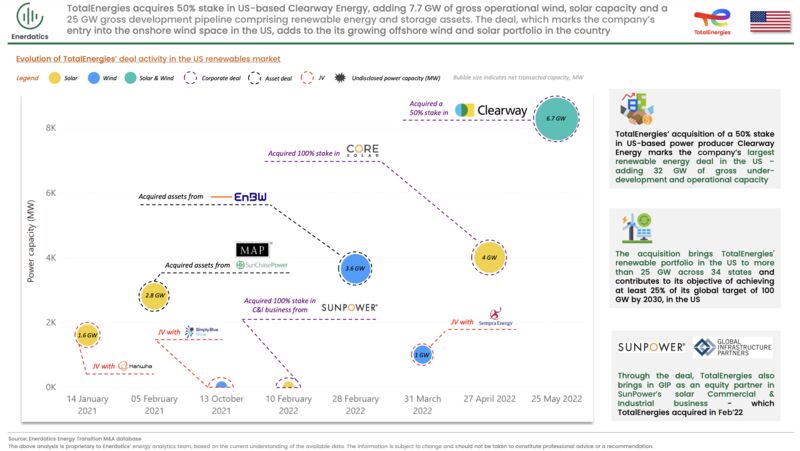

TotalEnergies has acquired 7.7 GW of gross operational non-regulated clean energy capacity in the United States, including 5.2 GW of wind and solar projects and 2.5 GW of conventional gas-fired generation facilities. Long-term power purchase agreements with utilities and corporate offtakers back these operational assets, with the majority of the contracts valid into the second half of the next decade. The transaction also includes a 25 GW development pipeline, which includes solar, wind, co-located, and standalone storage assets, 15 GW of which are in advanced stages of development. Clearway Energy owns a 42% stake in Clearway Energy Inc (CWEN), which results in TotalEnergies effectively acquiring 21% of CWEN, a listed affiliate that holds Clearway Energy’s renewable energy and conventional generation assets. Thus, the deal results in TotalEnergies adding ~1.1 GW of net operational and ~5.2 GW of net under-development renewable capacity to its portfolio, along with 0.5 GW of operational gas-fired power.

The consideration involves a $1.6 billion cash payment from TotalEnergies to private equity (PE) investor Global Infrastructure Partners (GIP). Further, GIP will receive a 50% stake in a TotalEnergies subsidiary that owns a 50.6% stake in SunPower’s commercial & industrial (C&I) solar business, which TotalEnergies acquired in February. Accounting for Clearway Energy’s and SunPower’s debt and equity capital, Enerdatics calculates the transaction enterprise value (EV) to be $4.6 billion.

The transaction implies an EV/Revenue metric of ~21, making it the most valuable transaction in the last three years for a company primarily operating with renewable generating assets in the United States. The transaction implies an EV/MW multiple of 0.67, which is lower than the average for operational assets. Enerdatics believes this is due to the majority share of early-stage projects in the transaction, which accounts for 74% of the acquired portfolio. While the operational assets are cash flow accretive to the buyer, the significant expenditure required to advance the development pipeline skews the transaction's blended metric.

Beyond wind and solar, the company has expanded its presence in the US biofuels and CCS markets by forming strategic alliances with Sempra, Svante, and Clean Energy Fuels. Aside from renewables, the company is working to expand its LNG portfolio in the United States, seeing the country as a key growth market in its efforts to become a clean power producer.

PS: The above analysis is proprietary to Enerdatics’ energy analytics team, based on the current understanding of the available data. The information is subject to change and should not be taken to constitute professional advice or a recommendation.

Click to know more about Enerdatics' Renewable Energy M&A, Finance, PPA, and Projects databases.