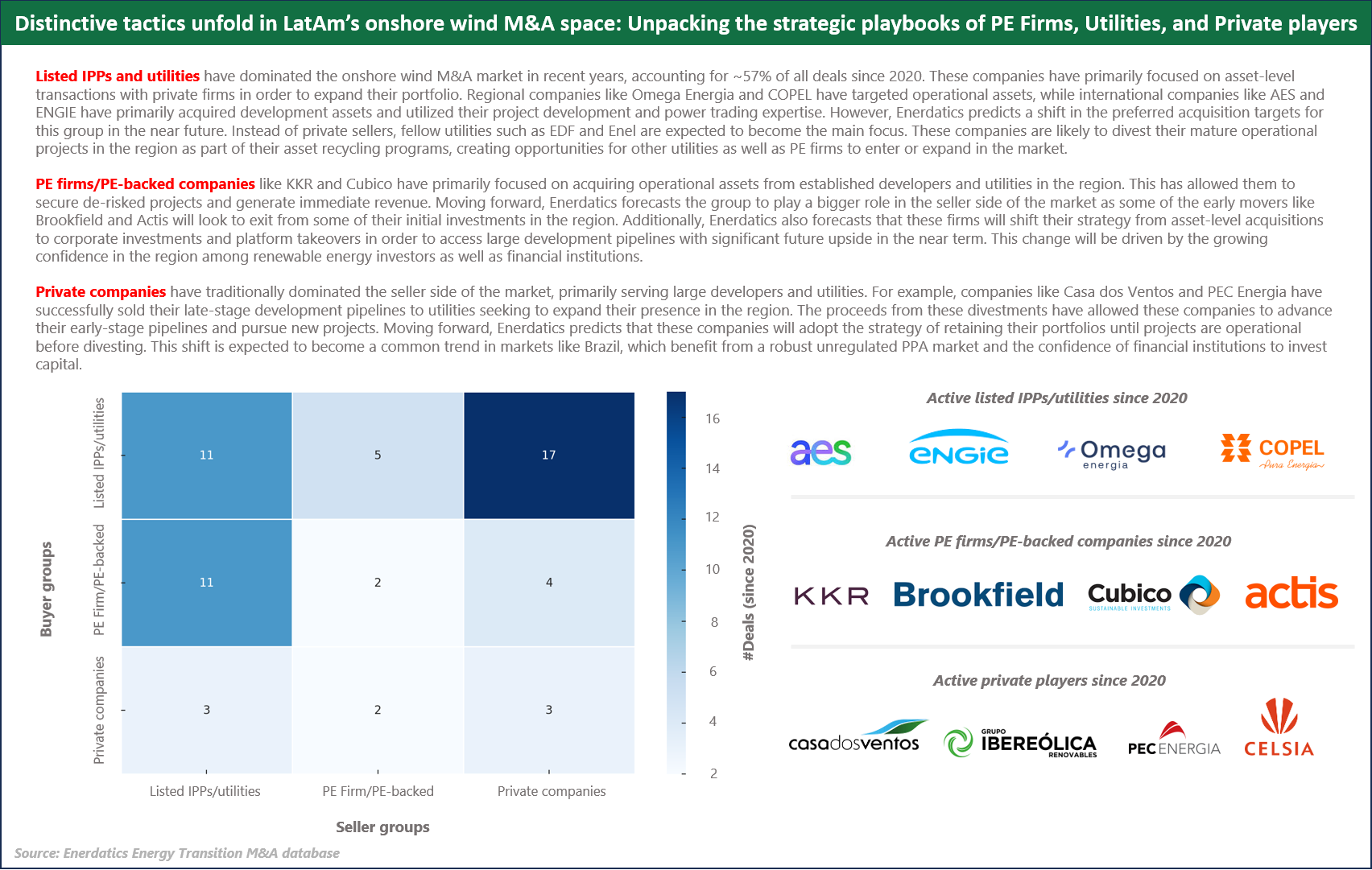

Listed IPPs and utilities have dominated the onshore wind M&A market in recent years, accounting for ~57% of all deals since 2020. These companies have primarily focused on asset-level transactions with private firms in order to expand their portfolio. Regional companies like Omega Energia and COPEL have targeted operational assets, while international companies like AES and ENGIE have primarily acquired development assets and utilized their project development and power trading expertise. However, Enerdatics predicts a shift in the preferred acquisition targets for this group in the near future. Instead of private sellers, fellow utilities such as EDF and Enel are expected to become the main focus. These companies are likely to divest their mature operational projects in the region as part of their asset recycling programs, creating opportunities for other utilities as well as PE firms to enter or expand in the market.

PE firms/PE-backed companies like KKR and Cubico have primarily focused on acquiring operational assets from established developers and utilities in the region. This has allowed them to secure de-risked projects and generate immediate revenue. Moving forward, Enerdatics forecasts the group to play a bigger role in the seller side of the market as some of the early movers like Brookfield and Actis will look to exit from some of their initial investments in the region. Additionally, Enerdatics also forecasts that these firms will shift their strategy from asset-level acquisitions to corporate investments and platform takeovers in order to access large development pipelines with significant future upside in the near term. This change will be driven by the growing confidence in the region among renewable energy investors as well as financial institutions.

Private companies have traditionally dominated the seller side of the market, primarily serving large developers and utilities. For example, companies like Casa dos Ventos and PEC Energia have successfully sold their late-stage development pipelines to utilities seeking to expand their presence in the region. The proceeds from these divestments have allowed these companies to advance their early-stage pipelines and pursue new projects. Moving forward, Enerdatics predicts that these companies will adopt the strategy of retaining their portfolios until projects are operational before divesting. This shift is expected to become a common trend in markets like Brazil, which benefit from a robust unregulated PPA market and the confidence of financial institutions to invest capital.

To gain a deeper insight into M&A trends at the corporate and asset level globally, request a trial of the Enerdatics Energy Transition M&A database today.

The above analysis is proprietary to Enerdatics’ energy analytics team, based on the current understanding of the available data. The information is subject to change and should not be taken to constitute professional advice or a recommendation.

Click to know more about Enerdatics' Renewable Energy M&A, Finance, PPA, and Projects databases.